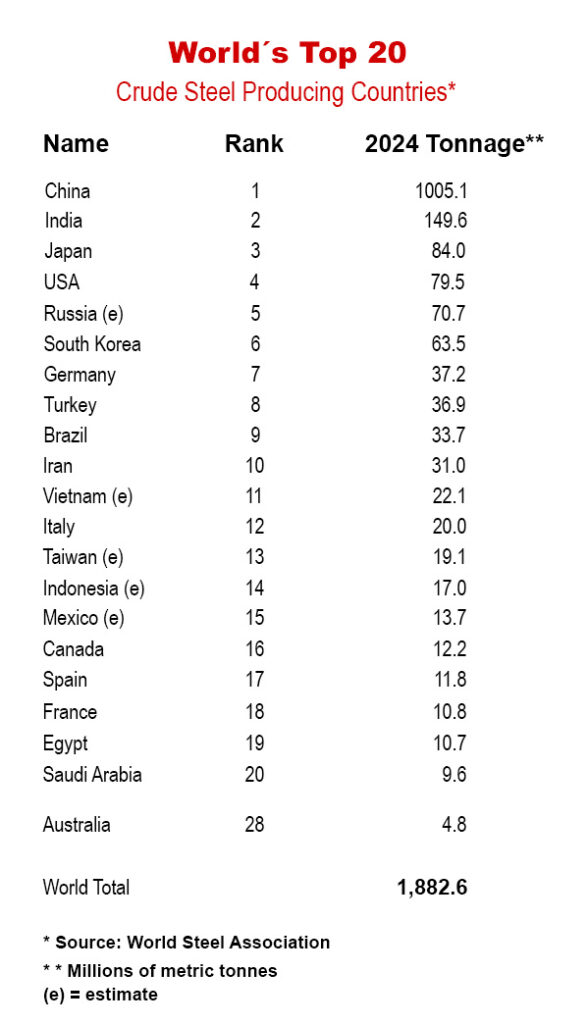

Although New Zealand’s steel industry is small by global standards, it is strategically vital to our nation’s economy and infrastructure. The centrepiece of our domestic steelmaking is New Zealand Steel Limited (NZ Steel), which is a wholly owned subsidiary of BlueScope Steel, and operates the Glenbrook steel mill, south of Auckland. Glenbrook produces around 650,000 tonnes of crude steel annually. It supplies the majority of flat-rolled steel and reinforcing products for the domestic construction, infrastructure, manufacturing and agricultural sectors. Historically, it has operated a unique ironsand and coal-based integrated steel mill, with emissions intensities similar to traditional blast furnaces. However, 2026 will see NZ Steel’s transition from the ironsand and coal processes to a state-of-the-art electric arc furnace (EAF). Often described as New Zealand’s largest single emissions reduction initiative, this evolution signals a long-term shift toward lower-carbon steelmaking. The project is currently in cold commissioning and is on track for operation in April / May of this year.

The new EAF furnace will use the highly renewable electricity grid and scrap steel, displacing coal and ironsand as majority primary inputs. This is a fundamentally different steelmaking route. Rather than reducing iron ore with coke and coal, an EAF melts recycled steel scrap using high-power electric arcs, providing greater operational flexibility and dramatically lower direct emissions. The project is expected to cut NZ Steel’s direct greenhouse gas emissions by 45-50%. This is about 800,000 to one million tonnes of carbon dioxide equivalent annually, which is the same as removing 300,000 cars from the road. Roughly speaking, it is 1% of New Zealand’s annual national emissions. The Glenbrook EAF is a $300 million capital investment co-funded by NZ Steel and the New Zealand Government via the Government Investment in Decarbonising Industry (GIDI) Fund; with the government contributing up to $140 million of the total cost.

Another step forward in 2026 will be the effect of policy reforms aimed at speeding up major projects and addressing an accumulated infrastructure deficit. In late 2025, the Fast-track Approvals Act 2024 came into force, establishing a permanent fast-track regime for infrastructure and development projects deemed to have regional or national benefits. This regime consolidates resource consent and related approvals to accelerate delivery timelines and reduce regulatory friction. Projects already approved under this process include quarries, ports and mining expansions, with more expected across energy, transport, housing and industrial sectors. With the 2025 Budget having allocated billions of dollars to infrastructure through health, schools, transport and housing, overall government capital investment remains substantial. Clearly, steel consumption in New Zealand tracks the infrastructure, construction and manufacturing industries.

In New Zealand, domestic production already satisfies a large portion of basic distribution steel and reinforcing steel demand. However, the new procurement policy emphasising the economic benefit to New Zealand will presumably boost domestic sourcing for government infrastructure projects, reinforcing bar and structural steel use from domestic mills, such as Pacific Steel (which sources billets tied to Glenbrook outputs). Steel & Tube and other NZ-based manufacturers of cut and bend reinforcing steel and mesh will be well positioned to support the procurement policy guidelines. That said, imported steels will no doubt continue to satisfy a significant proportion of demand, and their prices will reflect global input costs (such as iron ore and scrap pricing), exchange rates and import competitive dynamics.

To summarise: the New Zealand steel industry’s trajectory combines technological transformation with public-policy-driven decarbonisation, set against a backdrop of evolving infrastructure pipelines and climate pressures. Continued investment and regulatory clarity, especially around procurement, plus fast-track project delivery will shape the sector’s competitiveness and contribution to national economic goals. Major risks include energy pricing volatility, global raw material cost cycles, and potential delays in fast-track infrastructure delivery. It´s also worth remembering that the outcome of the general election in November could also bring some significant policy shifts, with consequent effect on our nation’s economic wellbeing.

Speaking of the economy, the rise in inflation to 3.1% for the 12 months to December 31 is not being seen by market observers as the beginning of a sustained upward trend; and expectations are that its next reading could well see a fall. Likewise, the steel industry will be buoyed by the 9.0% rise in new homes consented in the year to December 2025, as reported on February 3 by Stats NZ. Meanwhile, the slight tick up to 5.4% in national unemployment, announced on February 4, was not overly alarming.

Finally, Fletcher Building says it has entered into a binding agreement to sell its construction division, Fletcher Construction, to VINCI Construction for $315.6 million. VINCI Construction is a global leader in construction with 117,000 employees through 1,300 business units in about 100 countries. Commenting on the announcement, Fletcher Building´s managing director and chief executive officer, Andrew Reding, said: “Over the past year we have been clear that Fletcher Building’s future lies in being a focused building products manufacturer and distributor, supported by a strong balance sheet and disciplined capital allocation. The sale of Fletcher Construction is a significant step forward in delivering that strategy, while continuing the work underway to simplify the portfolio, lower debt and improve shareholder returns.”

The transaction is structured as the sale of Fletcher Construction Holdings together with its three New Zealand business units: Higgins; Brian Perry Civil; and Fletcher Construction Major Projects. Fletcher Construction’s South Pacific operations are excluded from the transaction. So too are residual responsibilities associated with Fletcher Construction’s completed legacy vertical construction projects, including the New Zealand International Convention Centre.

Gateway to the Australasian Steel and Metals Industry

Gateway to the Australasian Steel and Metals Industry